A week in which Swiss sensors found deep pockets, “boring” logistics became interesting, and Europe’s commercialization machine kept reminding everyone that market access is only the beginning.

Weekly snapshot of MedTech and Digital Health NEWS in Europe

People on the move

MedTech leadership: Coloplast

Coloplast named Gavin Wood as its next President and CEO, effective May 1. Wood joins from Johnson & Johnson MedTech EMEA with a reputation for steady-hand commercial execution rather than grand reinvention. In 2026, that is less a compromise than a strategy.

Money flows

MedTech funding: biosensing, cell therapy logistics, and rehab wearables

Biosensing funding

Xsensio (Switzerland)

$7M Series A.

Lausanne-based Xsensio closed an oversubscribed round led by WI Harper, with participation from Privilège Ventures, the European Innovation Council, and private investors across the US, Europe, and Asia.

The company is building a Lab-on-Skin platform for near real-time biochemical monitoring of proteins and hormones. Deeptech, yes. But the important part is that investors are still paying for platforms that might actually make it into clinical use.

Cell therapy logistics funding

Cellbox Solutions (Germany)

€3.5M, first tranche of Series A.

Cellbox raised fresh capital to expand its transport technology for living cells, with Companisto leading and NRW.BANK among existing backers.

Not the flashiest corner of medtech, but highly consequential: if cell therapy, organoids, and fertility workflows are going to scale, the logistics layer needs to grow up too.

Rehab wearables funding

Noxon (Germany)

multi-million-euro Seed round, amount undisclosed.

HTGF and Bayern Kapital led the round, joined by Auxxo and another institutional investor.

Noxon is working on a wearable muscle-computer interface for rehabilitation and neuromuscular care, a category where hardware, software, and clinical utility have to show up together or not at all. Europe’s investors are still backing hard technical bets when the use case is legible.

On the press

CE marks, robotic surgery expansion, and UK reimbursement policy

UK reimbursement policy | NICE

The UK government published its response on changes to NICE regulations on the cost-effectiveness threshold on March 3, 2026, confirming it will proceed with amendments that give the Secretary of State power to direct NICE on the standard threshold used in guidance development. This is not a device approval story, but it is a reimbursement-and-adoption signal that digital health and medtech founders selling into the UK should not ignore.

Cardiology / electrophysiology CE mark | Boston Scientific

Boston Scientific won an expanded CE mark in Europe for FARAPULSE, extending use of its pulsed field ablation platform to treat persistent atrial fibrillation. That matters because label expansion, not just first approval, is what starts turning a category winner into a broader standard of care. Europe remains a serious launch-and-scale market for electrophysiology.

Revello vascular device CE mark | BD

BD secured CE marking for the Revello vascular covered stent for common and external iliac artery lesions and said it will launch in CE mark-accepting European countries following its LINC 2026 debut in Germany. Another reminder that Europe still matters as a proving ground for procedural devices with a clean workflow fit. Familiarity, once again, is a strategy. Disclaimer: Author works at BD

Robotic surgery market expansion | Intuitive

Intuitive completed its acquisition of the da Vinci and Ion distribution business operated by ab medica, Abex, Excelencia Robótica, and affiliates, formally expanding direct operations across Italy, Spain, Portugal, Malta, San Marino, and associated territories. Less flashy than a new robot, but arguably more important: direct commercial presence is how medtech companies tighten service, training, and installed-base economics in Europe.

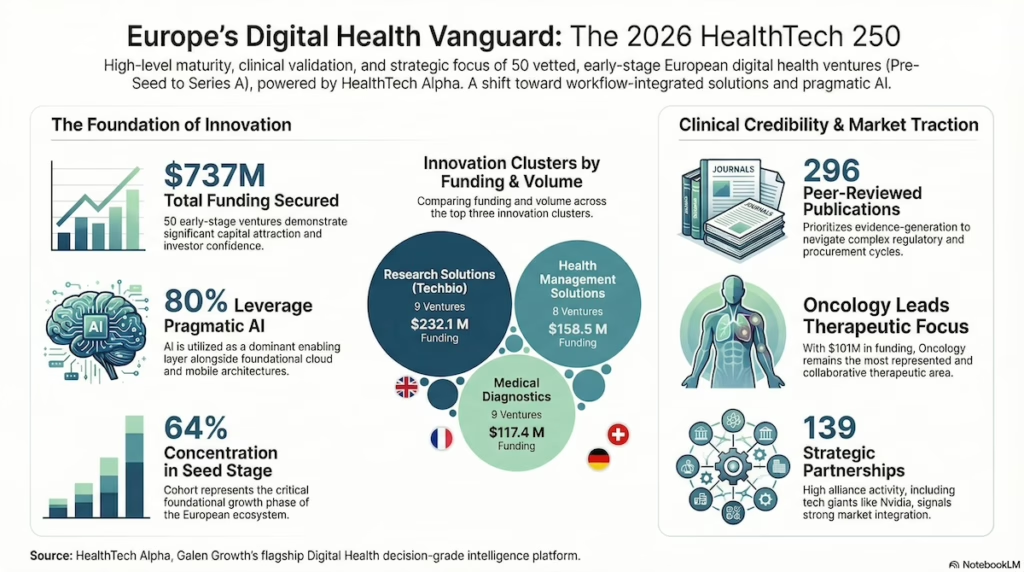

Digital health market map | Galen Growth

The new HealthTech 250 Europe 2026 cohort offers a useful counterweight to the gloomier venture narrative. Across the selected companies, Galen Growth reports 139 strategic partnerships, 296 peer-reviewed publications, and 40 regulatory approvals. The punchline for founders and investors: Europe’s digital health bench is increasingly evidence-backed, commercially connected, and harder to dismiss as slideware.

One thing to remember

The week in one line

Last week’s clearest pattern was not “more innovation.” It was better plumbing. Capital favored platforms and infrastructure that can survive contact with clinical reality, while commercial and policy moves pointed to the same conclusion: in European medtech and digital health, the winners are increasingly the teams that can monitor, deliver, train, reimburse, and scale, not just invent.