Europe Life Sciences Weekly Signal #35: Access Plumbing Becomes Strategy

Week of 27 April–3 May 2026

Europe had a useful reality check this week.

The strongest signals did not come from glossy AI claims, minor partnerships dressed up as strategy, or another ceremonial innovation slogan. They came from the machinery beneath growth: pricing, launch sequencing, regulatory support, evidence expectations, operating-model discipline, and whether Europe can remain a credible first-wave market for high-value innovation.

That may sound unglamorous. Good. This is where the commercial game is being decided.

The companies and systems that matter most this week are the ones asking a harder question: can science be turned into approval, reimbursement, adoption and scale fast enough to justify investment?

Commercial moves

AstraZeneca’s UK investment shows policy certainty still moves capital

AstraZeneca’s planned £300 million UK investment was the clearest capital-allocation signal of the week. Reuters reported that the investment follows the new US-UK pharmaceutical arrangement and will support sites in Cambridge and Macclesfield, including completion of the Rosalind Franklin building and digital “lab of the future” capabilities. The move also reverses earlier UK investment pauses, including a halted Cambridge project and a cancelled vaccine-manufacturing plan.

This is not just a UK industrial-policy story. It is a launch-economics story.

AstraZeneca also reported Q1 2026 total revenue of about $15.3 billion, up 8% at constant exchange rates, driven by double-digit growth in oncology and rare disease. The company reaffirmed full-year guidance, while Q1 oncology revenue remained the gravitational centre of its commercial model.

The commercial lesson is simple: investment follows markets where the route from approval to access is commercially intelligible. Europe can talk about competitiveness all it wants. Boards will still follow the money, the timelines and the pricing logic.

Chiesi buys KalVista — rare disease is becoming an infrastructure game

Chiesi’s agreement to acquire KalVista for approximately $1.9 billion adds EKTERLY / sebetralstat, an oral on-demand therapy for hereditary angioedema, to its rare immunology portfolio. KalVista said the deal is expected to close in Q3 2026, subject to customary conditions.

The obvious read is “rare-disease portfolio expansion.”

The better read is rare-disease commercial infrastructure.

In HAE, the product is only part of the business. The moat is built through diagnosis pathways, specialist relationships, patient services, rapid access, payer confidence and the ability to translate clinical differentiation into daily patient and physician behaviour.

For mid-sized European pharma, this is the takeaway: specialisation only scales if the operating model scales with it.

Novartis shows the cost of patent erosion, even when the launch portfolio is working

Novartis reported Q1 2026 net sales down 5% at constant currencies, with US generic erosion offsetting strong priority-brand momentum. Priority brands still performed strongly — Kisqali, Pluvicto, Scemblix, Leqvio and others posted high growth — but the legacy revenue drag was large enough to dominate the headline.

Reuters added the sharper commercial detail: Entresto sales fell 42% after US patent loss, with European patent expiry still ahead.

That is why this quarter matters. Novartis is not failing to launch. The issue is whether launch momentum can absorb legacy erosion quickly enough.

This is the operating-model test facing much of pharma: can companies run multiple high-growth priority assets with enough evidence, access, field orchestration and country sequencing to offset what the patent cliff removes?

Sanofi’s CEO transition is a delivery test, not a poetry contest

Sanofi shareholders approved the appointment of Belén Garijo as director and CEO, with her taking office on 1 May 2026. Sanofi framed the mandate around execution discipline, capital allocation and translating science into sustainable performance.

That language matters.

Sanofi does not need a more fashionable narrative. It needs sharper prioritisation, more consistent execution and proof that its immunology, vaccines and specialty-care ambitions can translate into commercial productivity.

This is not a “new era” story. It is a delivery story.

Regulation and market access

EMA’s breakthrough-device pilot is small, but strategically important

EMA launched its pilot programme for breakthrough medical devices on 28 April 2026. The first phase covers class III devices and certain class IIb active devices, with selected manufacturers receiving free expert-panel support and priority scientific advice. The pilot will run in phases through 2027 and later expand to other device types, including IVDs.

This should not be oversold. Europe has not suddenly recreated the FDA breakthrough-device pathway.

But it is still one of the more important MedTech regulatory signals of the year because it acknowledges the problem that founders, incumbents and investors have been complaining about for years: Europe has struggled to give high-value medical-device innovation a predictable fast lane.

The commercial implication is blunt: regulatory pathway design is becoming part of go-to-market strategy.

EUDAMED is no longer a regulatory side project

The European Commission confirmed that the first four EUDAMED modules become mandatory from 28 May 2026: actor registration, UDI/device registration, notified bodies and certificates, and market surveillance.

For commercial leaders, this is not “RA admin.”

Bad device data, unclear ownership, inconsistent certificate tracking or weak affiliate readiness can become launch friction, tender friction, field-force embarrassment and revenue protection risk.

This is where ppx’s best line deserves to survive: Europe is building a two-speed regulatory architecture. Faster support for genuine breakthrough innovation, less tolerance for basic compliance sloppiness.

Elegant? No. Important? Painfully.

The UK is packaging regulation, access and industrial policy together

The MHRA reported that it met or exceeded statutory targets and highlighted progress in clinical-trials reform, AI regulation, rare-disease pathways, international partnerships and the MHRA-NICE aligned pathway.

This sits alongside the UK’s wider US-UK pharmaceutical partnership, which the government linked to improved NHS access, tariff certainty and incentives for new-medicine launches.

The UK signal is not that everything is fixed. NHS adoption capacity remains the brutal bit. But the strategic direction is visible: the UK wants to be seen as a coordinated access proposition, not merely a mid-sized reimbursement market.

That matters because companies do not compare countries only by market size. They compare them by friction-adjusted value.

AI, Digital & Infrastructure

EU AI money is moving underneath the user interface

The European Commission opened seven Digital Europe Programme calls worth €63.2 million, including €9 million for AI-powered image screening in medical centres and €24 million for digital-health services linked to the European Health Data Space.

This is a better signal than another hospital chatbot pilot.

The money is moving toward infrastructure, validation, interoperability and deployment rails. That is less exciting for conference stages and more useful for operators.

For digital health and MedTech AI companies, the message is clear: EU non-dilutive funding is starting to ask the same questions as commercial procurement — evidence, workflow, standards, data access and operational readiness.

WHO’s EU AI snapshot shows adoption is real, but governance is still catching up

WHO/Europe published a report on AI readiness across EU health systems. The report says 74% of EU countries report using AI in diagnostics and 63% use chatbots for patient engagement, based on data collected between June 2024 and March 2025.

That caveat matters. This is not proof that Europe has solved AI deployment. It is a direction-of-travel signal.

The real issue is that adoption is moving faster than workforce readiness, governance maturity, and operating-model redesign. That is exactly where most commercial AI programmes wobble: not at demo stage, but when someone asks who owns the workflow, the risk, and the measurable business outcome.

Veeva entering the S&P 500 is a quiet infrastructure signal

Veeva Systems is set to join the S&P 500 before market open on 7 May 2026, replacing Coterra Energy.

This is not a European story directly, but it is a life-sciences infrastructure story.

Pharma’s commercial, medical, quality and clinical operating systems are increasingly shaped by listed software companies with their own quarterly cycles, AI roadmaps and competitive pressures. Platform choices are no longer just IT decisions. They are governance decisions that compound across launch portfolios.

That is why the index inclusion matters. Not because it changes the industry overnight, but because it formalises how strategic the plumbing has become.

MedTech signals

GE HealthCare reorganises around integrated imaging and commercial growth

GE HealthCare announced that it is combining Imaging and Advanced Visualization Solutions into a new Advanced Imaging Solutions segment of around $14.6 billion, while also creating a broader global markets structure. Catherine Estrampes was appointed Chief Commercial and Growth Officer, and the company framed the move around execution, innovation and growth.

The narrow read is restructuring under margin pressure. Reuters reported that GE HealthCare also cut its annual profit forecast amid inflation and tariff pressure.

The better strategic read: large MedTech companies are moving away from hardware-platform silos toward integrated disease-state, imaging, AI and commercial-growth models.

That is where the sector is going. Devices, data, workflow and service models are converging. The companies that organise around that reality early will have an advantage over those still defending legacy segment boundaries.

CMR Surgical keeps building the European MedTech export case

CMR Surgical submitted a 510(k) application to the US FDA to expand Versius Plus into benign gynaecology procedures, including total hysterectomy, oophorectomy and salpingectomy. The company said the submission follows its FDA clearance for cholecystectomy and builds on global clinical experience.

The signal is not only an indication.

CMR is one of the clearest examples of a European-headquartered MedTech trying to build global clinical experience outside the US and then sequence into the US market with a targeted regulatory path.

For European MedTech leaders, that is worth studying. It is not a romantic “European champion” story. It is evidence sequencing, market sequencing and commercial patience.

Money Flows

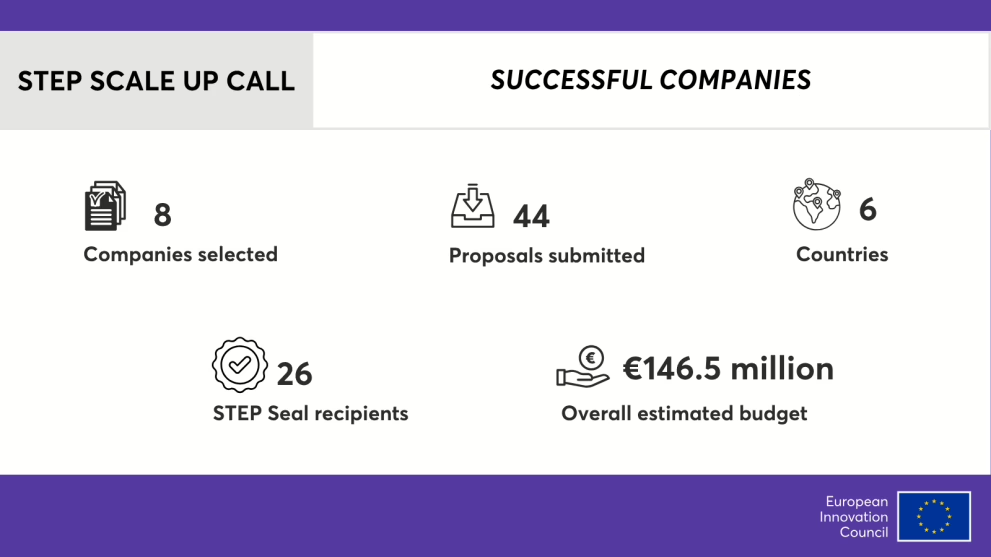

Aignostics shows Europe’s scale-up capital is becoming more strategic

The European Innovation Council selected eight companies for potential STEP Scale Up investments, with proposed equity tickets of €10–30 million each and a combined potential investment of €146.5 million, subject to due diligence.

Germany’s Aignostics was among the selected companies, with the EIC describing its work as transforming drug development and improving patient outcomes with AI.

This is not US-scale growth capital. But it is strategically relevant.

Europe is trying to fill the scale-up gap with more targeted capital in technologies it sees as strategically important. For life sciences AI, this reinforces a broader pattern: the winners will not be the ones with the cleanest demo. They will be the ones with deployable evidence, integrated workflows, credible partners, and a route to procurement

PIPELINE SIGNALS

Survodutide shows obesity is becoming a segmentation market

Boehringer Ingelheim and Zealand Pharma reported Phase III data showing average weight loss of 16.6% with survodutide after 76 weeks, versus 3.2% for placebo. Full data are expected at the American Diabetes Association Scientific Sessions in June.

The lazy read is: another obesity asset joins the race.

The better read is: obesity is becoming a segmentation market.

The next phase will not be judged only by percentage weight loss. Payers and clinicians will ask harder questions around cardiometabolic outcomes, liver disease, tolerability, discontinuation, lean-mass preservation, persistence and real-world pathway fit.

Survodutide still needs the full data package. But the strategic direction is clear: the obesity market is moving from “who loses most weight?” to “which patient, which outcome, which pathway, which cost?”

CHMP reminds us that evidence strategy is indication-specific

EMA’s April CHMP meeting recommended five new medicines for approval, including tolebrutinib for non-relapsing secondary progressive multiple sclerosis, onasemnogene abeparvovec for spinal muscular atrophy, and plozasiran for familial chylomicronaemia syndrome.

The point is not the count. The point is the pattern.

European evidence strategy is becoming more specific, more segmented and more commercially consequential. “Strong science” is not enough. The question is whether the evidence package supports the exact label, access story and adoption pathway the company needs.

Commercial and market-access teams that join late will keep discovering that the launch was already half-decided before they entered the room.