European MedTech Commercialisation Is Breaking at the Operating Model Layer

The European MedTech launch model is not failing because clinicians stopped caring about innovation. It is failing because the buying system changed faster than the commercial operating model around it.

When a European MedTech launch misses its number, the review usually lands on familiar explanations: pricing pressure, reimbursement delay, procurement friction, competitor response, or slower-than-expected clinical adoption.

Most of those explanations are real. They are also often downstream symptoms. The deeper issue sits one layer lower, in a commercial model built for a buying process that no longer exists.

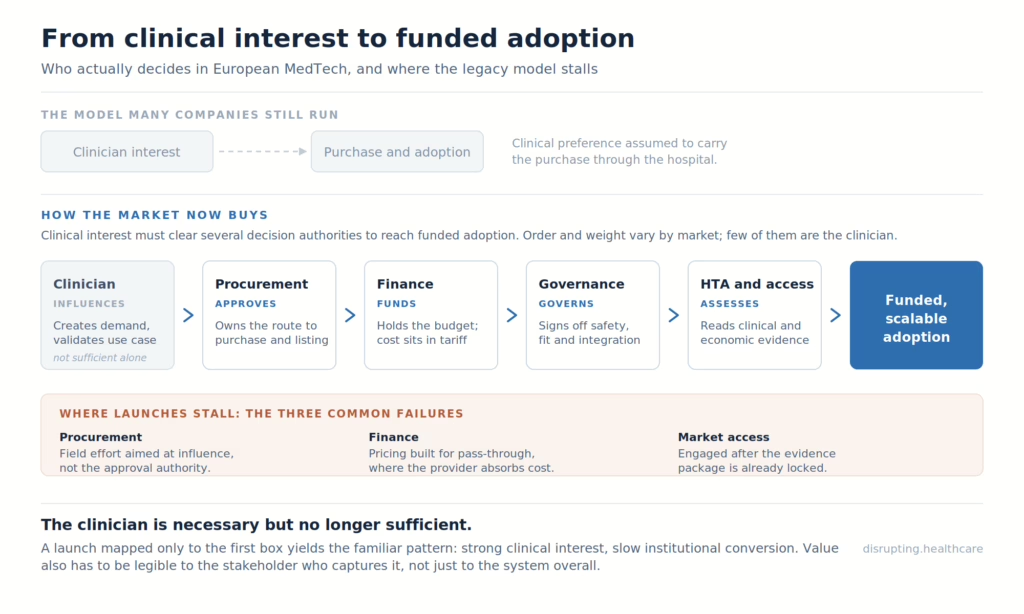

For years, the dominant European MedTech go-to-market model was built around clinical pull. Win the surgeon, interventional cardiologist, radiologist, specialist nurse, or department head. Build advocacy. Support evaluation. Give the field force enough access, enough clinical evidence, and enough persistence, and the product could move through the hospital.

That model worked because the buying process matched it. Clinical authority sat close enough to the budget. Procurement was often local enough to be influenced by departmental demand. Many legacy categories rewarded incumbency. Relationships were not the whole strategy, but they could carry a lot of commercial weight.

That world has not disappeared entirely. In some specialist, low-volume, or procedure-led segments, the clinician champion remains critical. But in major European markets, clinical support is increasingly necessary and insufficient.

The clinician can still create demand. They can validate the use case. They can shape specifications and support adoption. But they often cannot approve the budget, bypass a procurement framework, create reimbursement coverage, or carry the economic argument alone.

That is where European MedTech commercialisation is now breaking.

The old MedTech launch model was built around clinical pull

For years, the dominant European MedTech go-to-market model was built around clinical pull.

A specialist saw value in a device. The representative supported the evaluation. Early users created internal confidence. Procurement followed, sometimes slowly, but still within a structure where clinical demand could push the purchase forward.

The model rewarded field relationships, clinical education, peer advocacy, and local account navigation. It also rewarded incumbency. Once a product became embedded in a department’s routines, switching carried clinical, operational, and emotional costs.

That is why many MedTech companies built strong commercial organisations around access to clinicians. The representative was not merely a sales channel. In many categories, the representative was the connective tissue between the company and clinical practice.

But the launch model was always dependent on one assumption: that clinical preference could be converted into institutional adoption.

That assumption is now weaker.

In today’s European systems, the clinician can still create demand. They can validate the use case. They can help specify requirements. They can explain where the product fits in the pathway.

But they often cannot approve the budget. They cannot bypass a framework. They cannot create a reimbursement code. They cannot carry a health-economic argument alone. They cannot resolve cybersecurity, interoperability, data governance, or procurement questions for connected technologies.

That is where the old model breaks.

It asks the clinician to carry a commercial burden that the system has moved elsewhere.

Procurement has become a commercial strategy issue

The first shift is procurement. Across major European health systems, buying authority has become more consolidated, more formal, and more evidence-sensitive.

France is a useful example. The groupements hospitaliers de territoire were created by the 2016 health-system modernisation law to group public hospitals within territories. One of the delegated functions is purchasing, managed through a designated support hospital on behalf of the group. That does not make every French hospital purchase identical, but it does change the commercial entry point.

England has its own version of the same shift. NHS Supply Chain manages sourcing, delivery, and supply for more than 620,000 products for NHS trusts and healthcare organisations, while Integrated Care Boards shape local commissioning and adoption decisions. For suppliers, this means the market is not simply a set of individual trust relationships. Frameworks, national supply routes, and local adoption logic all matter.

Germany is different again. Hospital reimbursement is strongly shaped by DRG logic. Where a new method is not yet adequately covered by the existing system, companies may need to understand the NUB route, which allows hospitals to apply for temporary supplementary reimbursement for new examination and treatment methods.

The practical implication is simple: the stakeholder map has changed.

A launch plan built around clinician access alone is incomplete. It needs to map who influences use, who approves purchase, who controls budget, who assesses evidence, who carries operational risk, and who benefits economically from adoption.

Many underperforming launches have good answers to the first question. The stronger launches have specific answers to all of them.

MDR has pushed evidence into the commercial conversation

The second shift is evidence.

EU MDR is usually treated as a regulatory story, and rightly so. The regulation raised expectations around clinical evidence, post-market surveillance, documentation, and lifecycle management. But its commercial effect is just as important.

The evidence threshold has moved closer to the sale.

MedTech Europe’s 2022 MDR survey found that 54% of respondents did not intend to transition some of their portfolio to MDR. Among companies planning portfolio reductions, the expected discontinuation was roughly one-third of devices.

The same survey also reported certification timelines of 13 to 18 months through MDR-designated notified bodies.

The point is not that “half of the devices disappeared.” That would be too crude. The point is that MDR has forced portfolio rationalisation and raised the baseline expectation for clinical evidence.

Commercial teams sometimes underestimate what happens next. Procurement committees, HTA bodies, and hospital governance teams become more comfortable asking questions that sound regulatory but behave commercially.

What evidence supports this product?

Which patient population was studied?

Does the benefit translate into our setting?

What happens if we adopt this across a hospital group, not only in one department?

What cost does it add, remove, or shift?

A sales narrative that worked in a relationship-led market may still open the door. It rarely closes the institutional decision.

EU HTA is selective, but the direction matters

The third shift is HTA.

This needs precision, because overstating it is a fast way to lose a market access reader.

The EU Health Technology Assessment Regulation did not make every medical device subject to a central European assessment from 2025. The Regulation started applying on 12 January 2025, initially to new oncology medicines and advanced therapy medicinal products. Joint clinical assessment for selected high-risk medical devices and selected Class D in vitro diagnostics began in 2026.

For most device categories, this is still early and selective. The 2026 HTA work programme expects only around five joint clinical assessments of selected high-risk medical devices to be initiated.

But the commercial direction is clear. Evidence assessment is becoming more structured, more visible, and more likely to influence national payer interpretation. Member States still make reimbursement and pricing decisions, but the clinical evidence conversation is becoming harder to localise.

That changes launch timing. If payer-relevant evidence will be read across markets, market access cannot start after CE marking. It has to influence evidence planning before the file is locked.

The UK is not a simple “separate regulatory route” story

The UK adds another layer of planning complexity.

Some European launch plans still treat Great Britain as a clean post-Brexit regulatory separation: EU route on one side, UKCA on the other. In practice, the picture is more fluid.

CE-marked devices remain accepted on the Great Britain market under current transitional arrangements, with timelines depending on certificate type and regulatory status. In February 2026, the MHRA also opened a consultation on the indefinite recognition of CE-marked medical devices in Great Britain. As I write this article, the feedback is being analysed.

The commercial implication is not simply “build a separate UKCA dossier.” It is that GB market access remains a moving policy target. Companies need to track regulatory recognition, NICE evaluation, NHS procurement routes, funding mandates, and local adoption logic together.

A regulatory answer is not the same thing as a commercial route to adoption.

Where the legacy model breaks

The failure usually does not announce itself on launch day.

At launch, everything can look reasonable. The clinical story is strong. The sales team is trained. The first accounts show interest. KOLs are supportive. Internal confidence is high.

Then adoption is slower than expected. The opportunity pipeline becomes strangely thin. Sales cycles extend. Procurement asks for evidence the team cannot produce quickly. Finance challenges the price. Reimbursement takes longer than the business case assumed. A competitor with a weaker product but a better access model starts winning institutional conversations.

Eventually someone calls it market resistance.

Often, it is model resistance.

The market is resisting the way the company is trying to enter it.

At that point, the company does not need a better launch slogan. It needs a better launch architecture.

Three failure modes show up again and again.

Field effort aimed at the wrong centre of gravity

The team spends too much time with people who influence usage but do not control approval. The clinician remains important, but the pathway to purchase now runs through procurement, finance, clinical governance, and sometimes external assessment. If the account plan does not reflect that, activity goes up while conversion stays flat.

Pricing built for the wrong payment logic

A price that makes sense when cost can be passed through may fail when the hospital absorbs the incremental cost inside a fixed tariff. This is particularly important in hospital-based technologies where reimbursement mechanics determine whether clinical value can be converted into institutional willingness to pay.

Health economics has become a front-line commercial capability

One sign of an outdated commercial model is where HEOR sits.

In the old version, health economics often supported the commercial strategy. It helped build dossiers, validate claims, and prepare payer arguments when needed. Useful, but downstream.

That sequencing is increasingly wrong.

In the European MedTech market access, health economics has become a front-line commercial capability. The commercial team needs to explain not only what the technology does clinically, but what it changes economically.

Does it reduce complications?

Does it shorten the length of stay?

Does it move care to a lower-cost setting?

Does it reduce staff burden?

Does it improve throughput?

Does it prevent downstream interventions?

Does the stakeholder paying for the product capture the benefit?

That last question is often decisive.

A product can create system value and still face adoption friction if the budget holder does not capture that value. A hospital may pay more while the payer saves later. A department may absorb workflow disruption while the system benefits elsewhere. A clinician may see better outcomes while procurement sees only unit cost.

The commercial job is to make value legible to the stakeholder who has to act on it.

That is not a brochure problem. It is an operating model problem.

Country-specific models beat pan-European templates

“European launch strategy” is often used as if Europe were one commercial system with local variations.

That is convenient. It is also wrong.

Germany, France and England illustrate the problem.

In Germany, a hospital method that is not adequately reflected in existing DRG reimbursement may need the NUB route. Where high-risk devices are involved, the G-BA’s §137h procedure can assess methods involving medical devices of high-risk class for their medical benefit.

In France, reimbursement for many medical devices depends on LPPR listing, with clinical value assessed by CNEDiMTS at HAS. After the HAS assessment, CEPS is involved in setting the tariff and price before reimbursement by health insurance.

In England, adoption may involve NICE evaluation, procurement through NHS Supply Chain, local commissioning, and the MedTech Funding Mandate, which is designed to accelerate access to selected clinically effective and cost-saving technologies.

These are not cosmetic differences. They change launch timing, evidence needs, pricing logic, stakeholder mapping, and revenue assumptions.

A German reimbursement strategy does not become a French strategy because the product is the same. An English adoption route does not become a Nordic procurement route because the clinical need is similar. Localisation of messaging is not enough when the underlying market architecture is different.

The cost of building country-specific playbooks is real.

The cost of pretending one European model can stretch across all major markets is higher.

What to rebuild before launch?

The rebuild is not primarily a sales reorganisation. It is a redesign of how commercial strategy is built, who owns which decisions, and what evidence the organisation generates before launch pressure begins.

Before entering a priority market, the launch team should be able to answer five questions.

First, what is the actual decision pathway from clinical interest to funded adoption?

Second, which stakeholders can influence, approve, block, fund, or delay that pathway?

Third, what clinical, economic, operational, and technical evidence does each stakeholder need?

Fourth, what reimbursement timing should the revenue forecast actually assume?

Fifth, how will commercial, medical, regulatory, market access, HEOR, and technical teams make decisions together when the market does not behave like the central launch plan?

If the answers are vague, the organisation is not launch-ready. It is activity-ready.

An activity-ready organisation can train the field, prepare materials, brief KOLs, and open accounts.

A launch-ready organisation knows how the product becomes fundable, defensible, adoptable, and scalable inside each target market.

That distinction matters more than most launch plans admit.

The commercial model is now part of the product

European MedTech commercialisation is no longer won by asking whether the product is good enough.

That remains the first question. It is not the last.

The market now asks whether the product can be funded, procured, justified, integrated, and scaled inside a constrained health system. That means the commercial model is part of what the buyer is evaluating.

A strong device with a weak market access model will underperform. A strong clinical claim without an economic argument will stall. A clinician-led launch without procurement fluency will lose momentum. A central European playbook without country-specific architecture will look efficient internally and break externally.

The product may not be the problem. But the product will still carry the consequences of a model mismatch.

The companies pulling ahead are not simply the ones with the largest field forces or the best clinical relationships. They are the ones rebuilding European MedTech go-to-market around how the market now buys: evidence first, procurement-mapped, country-specific, economically literate, and integrated across commercial, medical, regulatory, market access, and HEOR.

That work is slower than campaign execution. It is less visible than the launch theatre. It is also where the number is won or missed.

One Thing to Remember

The binding constraint in European MedTech commercialisation has moved from clinical enthusiasm to institutional adoption.

Clinicians still matter. They always will. But in major European markets, a clinician champion is no longer enough to carry a product through procurement, reimbursement, evidence review, and budget approval.

A launch model built for the old world will keep producing the same pattern: strong interest, slow conversion, extended sales cycles, and post-mortems that blame the market for a decision architecture the company did not map early enough.

The better question is no longer only, “Who wants this product?”

It is, “What has to be true for the system to adopt it?”

References:

- MedTech Europe. MedTech Europe Survey Report: Analysing the availability of medical devices in 2022 in connection to the Medical Device Regulation (MDR) implementation.

- European Commission. Joint Clinical Assessments under the EU Health Technology Assessment Regulation.

- European Commission / HTA Coordination Group. Health Technology Assessment — 2026 Work Programme.

- French Ministry of Health. La fonction achat de GHT.

- NHS England. Supplying to the NHS.

- NHS England. Medical Technology (MedTech) Funding Mandate policy guidance.

- Medicines and Healthcare products Regulatory Agency. Regulating medical devices in the UK.

- Medicines and Healthcare products Regulatory Agency. Medical devices regulations: targeted consultation on the indefinite recognition of CE-marked devices.

- InEK. Neue Untersuchungs- und Behandlungsmethoden (NUB).

- Gemeinsamer Bundesausschuss. Bewertung neuer Untersuchungs- und Behandlungsmethoden mit Medizinprodukten hoher Risikoklasse.

- Haute Autorité de Santé. Pathway of medical devices in France: Practical guide.

- G_NIUS / Agence du Numérique en Santé. Economic Committee for Health Products (CEPS).