Europe Life Sciences Weekly Brief – Sovereign Cloud, Biogen’s Apellis Bet, and Europe’s Tightening Execution Layer

Week of 30 March–5 April 2026 (#31)

This was a week of infrastructure hiding in plain sight. A sovereign-cloud launch, a large rare-disease acquisition, EU funding for generative-AI cancer research, and a cluster of regulatory deadlines all pointed to the same underlying shift: life sciences is moving from digital ambition to execution architecture.

Commercial Moves

BD launches Pyxis Pro and Incada Connected Care on sovereign cloud in Europe

BD launched its AI-enabled Pyxis Pro Dispensing Solution and Incada Connected Care Platform across Europe on April 1, with a 15-language rollout planned in the months ahead. BD said it will host the European deployment on the AWS European Sovereign Cloud.

Why it matters.

The headline is a medication-dispensing system. The more important signal is the architecture choice underneath it. Digital sovereignty has moved from legal footnote to procurement reality, especially where hospital systems want cloud scale without creating political or compliance exposure. For commercial leaders, the lesson is straightforward: in Europe, platform adoption increasingly depends on infrastructure design being credible before the functionality pitch even lands.

Disclaimer: Author works at BD

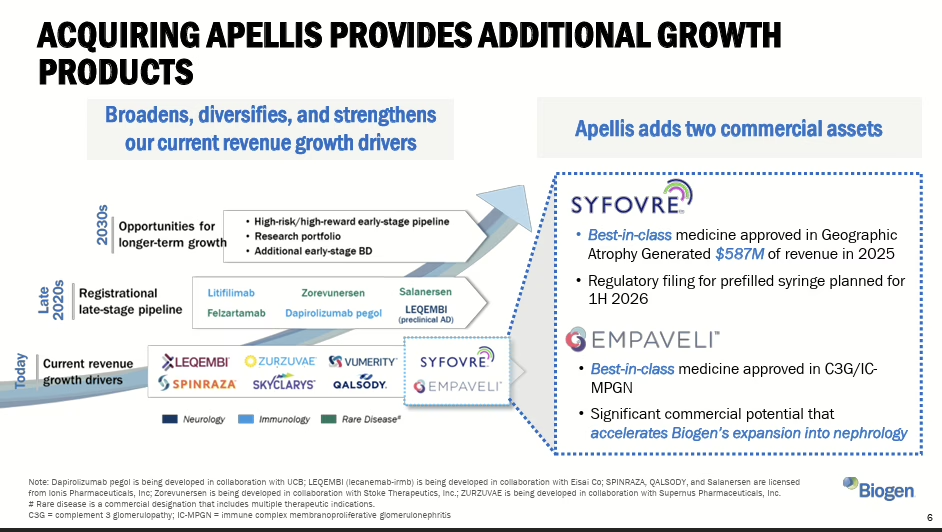

Biogen agrees to acquire Apellis Pharmaceuticals for $5.6 billion

Biogen agreed to acquire Apellis for roughly $5.6 billion in cash, adding two commercialised complement therapies (Empaveli and Syfovre) that generated $689 million in combined 2025 revenue. The deal strengthens Biogen’s position in nephrology and rare disease as it diversifies beyond its declining multiple sclerosis franchise.

Why it matters.

Targeted M&A is being used to buy specialist market access, field credibility and launch infrastructure in adjacencies where building organically would be slower and riskier. The question this raises for European commercial leaders is practical: when your next therapeutic area requires a new commercial infrastructure — specialists, channels, evidence routes — do you build or buy? In a market that preaches organic capability building, buying a ready-made commercial foothold is at least refreshingly honest.

Sanofi wins positive CHMP opinion for subcutaneous Sarclisa via on-body injector

Sanofi won a positive CHMP opinion for a subcutaneous Sarclisa formulation delivered via on-body injector in multiple myeloma. If approved, it would be the first anticancer treatment in the EU delivered through an on-body injector, with evidence supporting comparable efficacy and safety versus IV administration.

Why it matters. This is not a minor formulation tweak. It is a route-of-care shift with implications for site capacity, treatment convenience and how companies package therapy, device and experience as one commercial proposition. Expect more oncology players to rediscover that delivery innovation can be commercially material when infusion capacity is the real bottleneck.

AI and Digital Signals

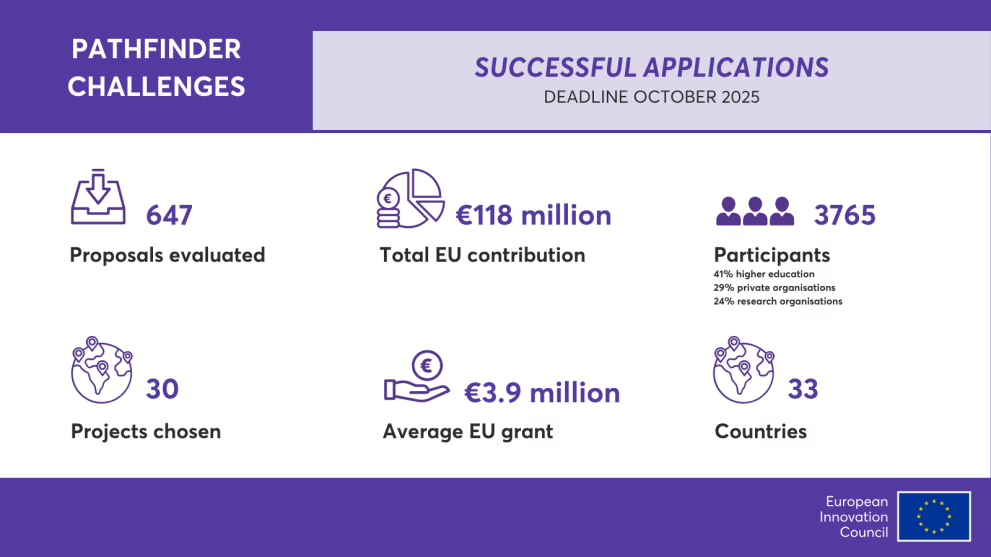

EIC awards €118 million to 30 breakthrough projects, including generative AI for cancer diagnosis

The European Innovation Council awarded €118 million under the 2025 Pathfinder Challenges call, selected from 647 submitted proposals. Two of the four challenge areas are directly relevant to life sciences: generative-AI agents for cancer diagnosis and treatment, and biotech for climate-resilient crops and biomanufacturing.

Why it matters.

This is early-stage research funding, not commercial deployment. That is precisely why it matters. Europe is still better at funding the science layer than the operating layer, but these programmes shape the capabilities that later move into diagnostics, workflow and evidence-generation models. Commercial teams should watch these funding streams less as immediate market signals and more as early indicators of where the next evidence and platform expectations will emerge.

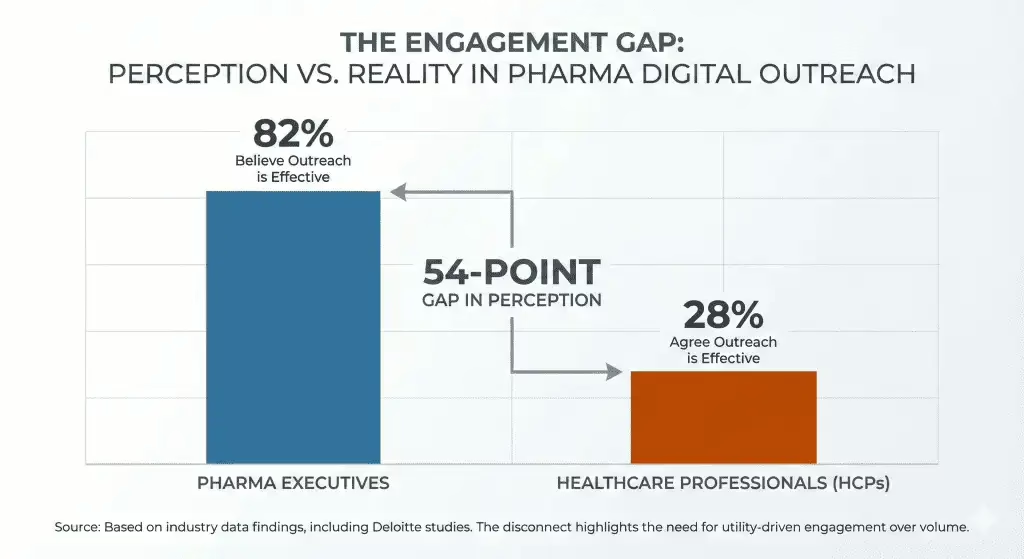

The HCP engagement perception gap is now quantified — and it is worse than most teams assume

A Medicine to Market analysis cites industry data showing 82% of pharma executives believe their digital outreach is effective, while only 28% of HCPs agree. Approximately 97% of digital outreach goes unanswered.

Why it matters.

The report argues that commercial teams are optimising for send volume rather than decision support. If 97% of your current volume is ignored, increasing that volume is not a strategy. For anyone leading omnichannel or commercial excellence in Europe, this is the data point that should reframe the 2026 operating plan: the metric must shift from reach to relevance.

AI story of this week is:

Governance, not magic

BD’s sovereign-cloud choice and the EIC’s cancer-AI funding are very different stories on the surface. Underneath, both point to the same constraint: AI in European healthcare only becomes commercially durable when the surrounding architecture is workable.

Why it matters.

Models are easy to demo. Operating conditions are not.

That is becoming the defining split in the market.

Regulation and Market Access

EUDAMED: four modules become mandatory on 28 May 2026

The European Commission has confirmed that four EUDAMED modules become mandatory from 28 May: actor registration, UDI/devices registration, notified bodies and certificates, and market surveillance. New MDR/IVDR devices must be registered before market placement from that date; legacy devices must be registered by 28 November 2026.

Why it matters.

For MedTech organisations, this is now operational infrastructure with direct effects on portfolio visibility, registration discipline and go-to-market readiness across the EU. No one will mistake it for an inspiring strategy deck. It will still determine who spends Q3 fixing preventable execution friction.

MHRA consultation on indefinite CE-mark recognition closes 10 April

The MHRA consultation on indefinite recognition of CE-marked medical devices in Great Britain runs until 10 April 2026. Around 90% of devices currently used in GB carry CE marking.

Why it matters.

If the UK continues in that direction, the practical gain is not abstract regulatory harmony. It is reduced duplication for manufacturers managing evidence, supply and launch sequencing across both EU and UK markets. The companies that benefit most will be the ones that treat this as a portfolio-planning question early, not as a legal update to skim later.

EU HTA: second 2026 request period for Joint Scientific Consultations opens

On 1 April, the Commission opened the second 2026 request period for Joint Scientific Consultations, with requests due by 29 April for both medicines and medical devices. Briefing document slots are available for July, August and September 2026.

Why it matters.

JSCs are designed to help developers shape clinical-study plans before a later Joint Clinical Assessment. Commercially, this is where market access, evidence strategy and development planning stop being separate workstreams. Teams that still bolt HTA thinking on near launch are about to pay for that habit.

MDR/IVDR simplification: feedback period extended to 6 May

The Commission’s targeted simplification proposal, published in December 2025, is still moving through feedback and legislative discussion. The public feedback period via the Better Regulation Portal has been extended to 6 May 2026. Key proposed changes include removing the fixed five-year certificate validity, expanding software classification provisions under a revised Rule 11, and reducing duplication between MDR/IVDR and the AI Act for AI-enabled medical devices. The Commission expects overall cost savings of approximately €3.3 billion per year.

Why it matters.

The direction is commercially important. But this is not yet the moment for dramatic claims about regulatory relief. The useful interpretation is simpler: Europe knows the current system is constraining competitiveness, and commercial planners should expect the regulatory operating model to keep evolving rather than settle any time soon

Weekly Signal

What Leaders Should Watch?

Infrastructure is becoming part of the commercial proposition.

Sovereign cloud, workflow fit and regulatory readiness are increasingly conditions of adoption, not back-office implementation details.

Portfolio expansion is being bought, not built, where time-to-credibility matters.

Biogen’s Apellis deal is a reminder that specialist access, therapeutic adjacency and commercial footprint can be acquired faster than they can be assembled.

Delivery model innovation is moving closer to commercial strategy.

Route of administration, site-of-care flexibility and workflow fit are becoming revenue and adoption questions, not just medical affairs detail.

Europe’s execution layer is tightening.

EUDAMED deadlines, HTA consultation windows, MDR/IVDR feedback periods and UK-EU device recognition choices are all pushing companies toward earlier coordination across regulatory, access and commercial teams.

Practitioner’s Lens

The week’s stories were not scattered. They all pointed to the same reality: the layer between strategy and execution is where value is now won or lost.

Sovereign cloud, targeted M&A, oncology delivery redesign, EUDAMED readiness and earlier HTA discipline all sit in that middle layer. That is why so many organisations feel busy but not faster.

AI will amplify the gap between well-structured organisations and messy ones.

It will not close it. In European life sciences, infrastructure is no longer support work. It is strategy with less flattering branding.

This content has been enhanced with AI