Europe Life Sciences Weekly Signal #45: The Moat Is Moving Beyond the Molecule

Week of 6–12 July 2026

Two British discovery platforms found larger pharmaceutical balance sheets this week.

Astex licensed compounds from its breast-cancer discovery programme to Genentech. Myricx Bio, spun out of Imperial College London and the Francis Crick Institute, agreed to be acquired by Novartis for up to $1.5 billion.

Both are commercial successes.

Together, they expose a structural weakness.

Europe created the science and captured transaction value. But the expensive next stages, clinical development, platform expansion, global commercialisation and lifecycle execution, will sit largely inside Genentech and Novartis.

Saying Europe has simply “lost” the science is lazy. Founders, universities, employees and investors have created and realised genuine value.

Pretending nothing structural has happened because the sellers were paid is equally lazy.

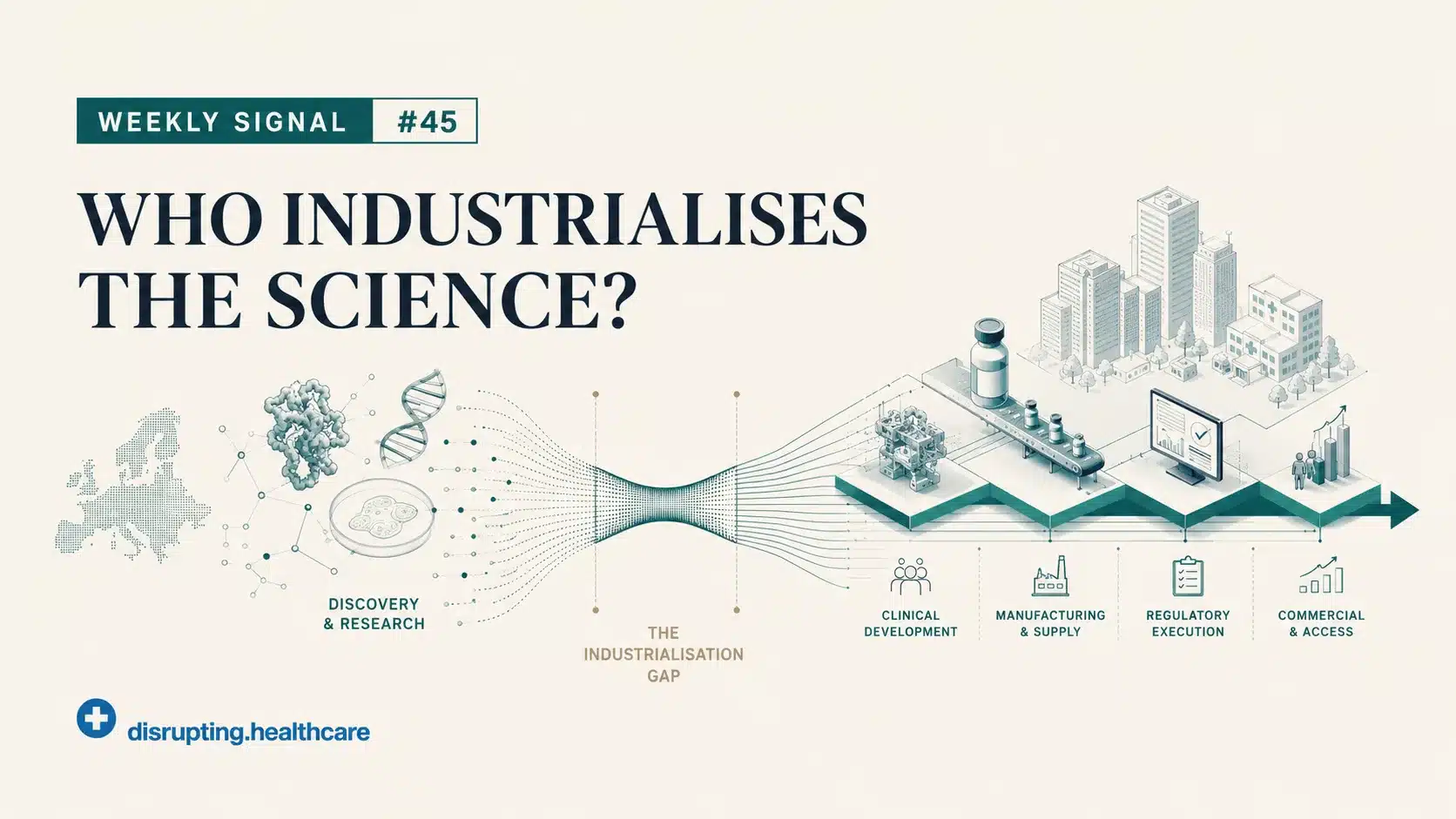

Europe remains very good at creating scientific options. It is less effective at building the industrial machine that exercises those options at global scale.

Elsewhere this week, Novo Nordisk started evaluating a drug-delivery platform it did not develop, while Brussels began constructing institutional capacity to evaluate advanced AI models.

The unifying question is no longer who can discover.

Europe answered that twice.

The question is who industrialises.

IN THIS ISSUE Myricx–Novartis • Astex–Genentech • Novo–Vivani • EU AI • Practitioner’s Lens

Key Signals

Novartis buys a possible ADC payload class, not one product.

Myricx’s proposed $1.5 billion acquisition shows the premium attached to distinctive European science and the larger balance sheets required to develop it at global scale.

Astex makes the R&D transfer point a strategic decision.

Astex retains milestone and royalty economics while Genentech assumes the expensive development and commercialisation burden.

Novo evaluates treatment architecture, not “twice-yearly Wegovy”.

The implant remains early. Its commercial value will depend as much on procedure capacity, reversibility and pathway economics as on dosing frequency.

Europe buys more AI runway while building evaluation capacity.

The 2028 MedTech date matters, but AI literacy, GPAI and transparency obligations are already live or arriving much sooner.

Commercial Moves

Myricx turns a UK discovery platform into a Novartis industrialisation bet

$1.1bn upfront

Up to $400m in milestones

Preclinical ADC payload platform

On 6 July, Novartis announced an agreement to acquire Myricx Bio for up to $1.5 billion.

The proposed transaction comprises $1.1 billion upfront and up to $400 million in potential milestone payments. Completion is expected in the second half of 2026, subject to regulatory approvals and other customary conditions.

Myricx is developing a potentially first-in-class antibody-drug conjugate payload platform based on inhibition of N-myristoyltransferase, or NMT. Its two lead ADC programmes target B7-H3 and HER2.

The attraction is not another antibody attached to another familiar chemotherapy payload.

Many current ADC programmes rely on a relatively narrow group of payload classes. Myricx’s NMT inhibitor approach is designed to offer a different mechanism, including potential activity in models resistant to commonly used TOPO-1 payloads.

Novartis is therefore buying a platform and a possible payload class, not merely one product. Its transaction announcement explicitly describes the acquisition as an opportunity to scale an innovative platform.

That wording matters.

Myricx was founded in 2019 from research at Imperial College London and the Francis Crick Institute, with support from Cancer Research UK. It was initially seeded by Sofinnova Partners and Brandon Capital and raised a £90 million Series A in 2024.

This is a strong result for the British translational ecosystem.

Academic research became a company. Specialist investors funded it. The team changed direction from conventional small molecules to ADC payloads. A global pharmaceutical company then offered substantial capital before the platform entered clinical development.

That is not failure.

It is also not industrial scale remaining in Britain.

The exit value is being realised in the UK ecosystem, but the next phase of development, platform expansion and eventual global commercialisation will take place inside Novartis.

That distinction is the policy signal.

The European Commission’s biotechnology analysis shows that the European Economic Area’s share of global commercially sponsored clinical trials fell from 22% in 2013 to 12% in 2023. China’s share rose from 5% to 18% over the same period.

One acquisition does not explain that decline.

It is, however, consistent with the same structural pattern: Europe produces substantial science but has fewer organisations able to finance and operate its development at global scale.

For operators, this is not an invitation to mourn every acquisition.

It is an instruction to decide where the organisation genuinely competes.

A discovery company should become exceptionally good at creating, validating and transferring assets. It should price the handover deliberately rather than drift towards a transaction after its financing options narrow.

An industrialising company should become exceptionally good at absorbing external science and making it worth more inside the organisation than outside it. That requires clinical operations, CMC, regulatory strategy, evidence generation, market access, launch execution and lifecycle management to function as one machine.

Both models are legitimate.

The expensive mistake is pretending to be both without sufficient capital or scale to excel at either.

Astex shows why the handover point is now a strategic decision

On 6 July, Astex Pharmaceuticals entered an exclusive worldwide research collaboration and licence agreement with Genentech covering small-molecule candidates against a cell-cycle-dependent target in breast cancer.

Astex is granting Genentech an exclusive licence to compounds from an existing discovery programme. The companies will work together to optimise the lead compounds and identify preclinical candidates.

Genentech will then assume sole responsibility for preclinical development, clinical development and global commercialisation.

Astex receives $25 million upfront and could receive further preclinical, clinical, regulatory and sales milestone payments taking the potential total above $490 million, plus tiered royalties.

The programme originated in earlier work involving Astex, Newcastle University and Cancer Research Horizons.

This is not European science being given away.

Astex has monetised its discovery capability, retained substantial downstream economics and transferred capital-intensive execution risk to one of the industry’s strongest development organisations.

But it is a deliberate division of labour.

Astex owns the specialist discovery engine. Genentech owns the balance sheet, development infrastructure and global commercial system needed to turn that chemistry into a medicine.

The strategic question is therefore not whether external innovation is replacing internal R&D. Large pharmaceutical companies have licensed science for decades.

The question is where the handover should happen.

Transfer too early and the originator may surrender value before the programme is sufficiently validated. Transfer too late and a smaller organisation may spend years building capabilities that add cost without creating differentiation.

For R&D and portfolio leaders, that handover point should be designed as deliberately as the asset itself.

The useful test is simple.

Which activities increase the distinctiveness and value of the programme inside your organisation, and which become more valuable when moved into somebody else’s machine?

Internal ownership is not proof of strategic importance.

Sometimes the most strategic decision is knowing precisely where internal ownership should end.

Drug Delivery & Commercial Models

Novo Nordisk is evaluating treatment architecture, not “twice-yearly Wegovy”

On 7 July, Vivani Medical announced an agreement enabling Novo Nordisk to conduct a non-exclusive internal evaluation of NPM-139, Vivani’s semaglutide implant for chronic weight management.

There are no exclusivity provisions covering NPM-139 or Vivani’s NanoPortal technology.

Vivani describes the product as a miniature subdermal implant intended to support once- or twice-yearly administration.

The company had received approval to initiate a Phase I first-in-human study using Wegovy injections as an active comparator, but NPM-139 had not produced human clinical data.

The company announcement confirms that this is a non-exclusive evaluation. The agreement is also recorded in Vivani’s SEC filing.

The headline temptation is obvious.

“Twice-yearly Wegovy.”

Resist it.

This is not a licensing transaction, a development partnership or clinical evidence that a semaglutide implant works. Novo Nordisk has agreed to examine an early delivery technology.

That narrower description does not make the story less important.

It reveals where competition in obesity treatment may move next.

Weekly injections, daily tablets and long-acting implants create different patient experiences and entirely different commercial systems around the molecule.

An implant could reduce the behavioural burden of frequent dosing and potentially improve persistence. It would also require insertion and removal capacity, provider training, reimbursement for the procedure, patient-selection protocols and a clear route for stopping treatment when tolerability becomes a problem.

Convenience does not arrive alone.

It brings an operating model with it.

For payers, the eventual comparison would not be limited to implant versus injection. It would include drug cost, clinical time, persistence, discontinuation, monitoring, treatment waste and the consequences of patients moving on and off therapy.

For manufacturers, the delivery system could become a source of differentiation as GLP-1 pharmacology becomes more crowded.

But the device cannot be assessed separately from the pathway.

A treatment administered twice a year is only commercially superior when the infrastructure surrounding those two appointments works better than the infrastructure surrounding 52 injections.

Otherwise, it is simply a year of operational complexity delivered in one sitting.

AI & Digital Transformation

Europe bought more AI runway. The work has already started.

On 7 July, the European Commission presented its Action Plan on Cybersecurity and Artificial Intelligence.

The plan includes a call to expand EU capacity to evaluate advanced AI models before they enter the market. The Commission expects the new evaluation capacity to become operational in 2027.

The Commission and ENISA also plan to establish a secure testing platform through which organisations in critical sectors, including health, energy, transport, finance and public administration, can test and deploy AI systems more safely.

This marks a shift from writing AI rules towards building the institutions needed to apply them.

The lazy interpretation is that another AI compliance deadline is approaching.

The accurate interpretation is more complicated.

The European Parliament approved the Digital Omnibus changes on 16 June. The Council gave its final approval on 29 June, with publication in the Official Journal and entry into force following that approval.

The revised timetable creates two dates for high-risk AI obligations.

Standalone high-risk systems covered by designated use cases will be subject to the rules from 2 December 2027.

High-risk AI systems embedded as safety components in products covered by relevant EU sectoral legislation, including qualifying medical devices and diagnostics, will be subject to the rules from 2 August 2028.

For MedTech companies, 2 August 2028 is therefore the critical high-risk date for qualifying product-embedded systems.

But the delay does not mean the AI Act has disappeared until then.

AI literacy obligations have applied since February 2025. Rules for providers of general-purpose AI models became applicable in August 2025. Most transparency obligations concerning interactions with AI and AI-generated content apply from August 2026, with a specific transition to December 2026 for certain machine-readable marking requirements.

The Commission’s AI Act implementation page sets out the staged application of these obligations.

The correct executive summary is therefore not “the deadline has moved”.

It is that the heaviest product-related requirements have moved, several horizontal duties are already live or imminent, and Brussels is using the interval to build evaluation and testing capacity.

That should change the order in which life sciences companies approach AI governance.

Classification comes first.

A model embedded in a diagnostic device, a pharmacovigilance summarisation tool and a commercial next-best-action engine may have different intended uses, risk profiles and legal obligations.

Putting all three into one generic “responsible AI” programme may look organised.

It is not a regulatory classification.

Companies first need a reliable inventory of their AI systems, their intended purposes, the data they use, their owners and the decisions they influence. Only then can proportionate controls be assigned.

The revised timetable provides more runway for product-embedded systems.

It does not make the inventory shorter, the ownership clearer or the evidence easier to reconstruct later.

The extension bought preparation time.

Treating it as slack would be an unusually efficient way to waste it.

What Leaders Should Watch

The next handover point

Astex and Myricx reached different transactions at different stages. Watch where other European discovery companies transfer development responsibility and how much validation they achieve before doing so.

Platform prices before clinical proof

Novartis is committing $1.1 billion upfront to acquire a preclinical platform. That raises the strategic value of differentiated payload technology and the execution burden attached to platform acquisitions.

Delivery economics in obesity

The competition is no longer limited to weight-loss percentages. Administration frequency, service capacity, persistence, reversibility and total pathway cost will increasingly shape differentiation.

AI obligations that did not move

The 2028 date will dominate MedTech discussions. AI literacy, GPAI and transparency duties deserve more immediate attention because several are already applicable or arrive in 2026.

Practitioner’s Lens

The tempting summary is that European science is being sold off.

That is emotionally satisfying and analytically lazy.

What happened this week was a series of rational decisions about where different activities create the most value.

Astex chose to monetise a discovery programme while retaining milestone and royalty economics. Genentech assumes the downstream development and commercial burden.

Myricx’s shareholders accepted a substantial exit. Novartis is buying the opportunity to establish and scale a new ADC payload class.

Novo Nordisk is examining a delivery platform it did not build because internal invention is not the only route to treatment differentiation.

Each transaction makes sense on its own.

The structural problem appears when they are aggregated.

Europe repeatedly demonstrates strength in academic science, specialist discovery and early company formation. Its weakness becomes visible in the capital-intensive middle, where clinical development, manufacturing, regulatory execution and commercial scale must operate together.

That middle is often where a larger pharmaceutical balance sheet enters.

The result is not that Europe captures nothing.

It captures grants, research activity, employment, intellectual property, licence income, venture returns and acquisition proceeds.

What it captures less consistently is the compounding value generated by operating a successful platform through multiple clinical programmes, launches and lifecycle expansions.

That is the industrialisation gap.

European policy can improve the environment through financing instruments, clinical-trial reform, regulatory coordination and shared infrastructure.

Individual companies cannot wait for that environment to become ideal.

Their response has to be more precise.

Know which part of the chain creates differentiated enterprise value. Build disproportionately around it. Partner, license or transfer the rest while the organisation still has options and negotiating leverage.

Do not build functions merely because a conventional pharmaceutical organisation chart says they should exist.

A full value chain is not automatically a capable value chain.

Sometimes scale comes from owning more.

Sometimes it comes from knowing exactly what not to own.

One Thing to Remember