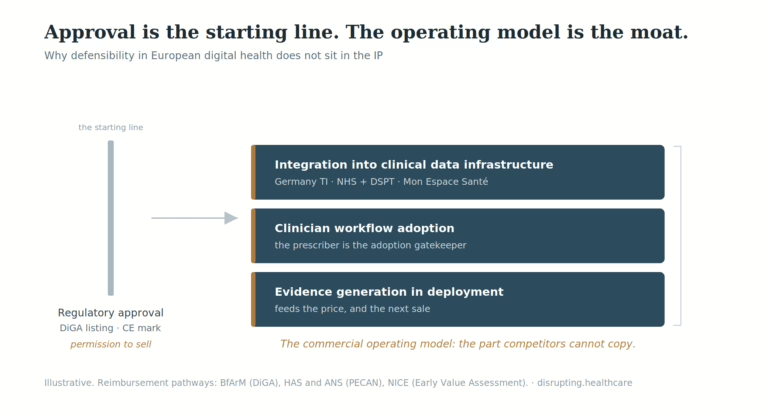

Digital Health Commercialisation in Europe: Why the Operating Model Beats the IP

Digital health companies love to talk about defensible technology. European health systems are much less romantic. They care whether the product gets used, fits the workflow, generates evidence, survives procurement and justifies reimbursement after the first enthusiasm fades. In Europe, a CE mark, a DiGA listing, a PECAN decision or a positive early value signal…