A compact week: venture debt fuels vascular access, cardiology gets a non-invasive CE mark, and NICE nudges digital rehab platforms toward the NHS.

People on the move

Lucile Blaise joins LivaNova (UK) as Global Head of Commercialization, Obstructive Sleep Apnea, adding strong EU market access chops to the executive team.

Money flows

Xeltis (NL) gets nearly €50M, venture debt + equity; package includes up to €37.5M from EIB (first €10M drawn) and €10M from existing investors EQT Life Sciences and Invest-NL. Funds push aXess vascular access conduit toward EU commercialization.

Angelini Ventures (Italy): €150M EIB co-investment agreement to back European biotech and digital health startups over six years (EIB €75M + Angelini Ventures €75M). Signals more institutional firepower for EU healthtech.

Annette (France) €2M round to scale its GLP-1 companion care platform for structured obesity support; led by Redstone, Ring Capital and AFI Ventures.

Ray Studios (France) €10M to expand its physician-led tattoo-removal clinic network across Europe; co-led by Factory Capital and Nickleby Capital.

On the press

• Cardiawave (FR): Valvosoft® receives CE Mark as the first non-invasive ultrasound therapy for severe symptomatic aortic stenosis; data cited from EU FIM and pivotal studies across 12 centres.

• Boston Scientific: European approval for the Farapoint™ pulsed-field ablation focal catheter to treat atrial fibrillation, complementing Farapulse™ PFA platform.

• NICE (UK) publishes Early Value Assessment (HTE35) for digital platforms supporting cardiac rehabilitation, enabling conditional NHS use while evidence is generated over three years.

One thing to remember

EU cardiology is having a moment: capital is flowing into commercialization-ready devices, while regulators opened the door to earlier adoption of digital rehab and cleared a novel non-invasive therapy. Founders who can pair strong clinical data with payer-relevant outcomes will find both financing and fast-track pathways this winter.

Where the regulations help, the funding flows, and the pilots don’t take geological time

If you ask ten founders where to launch a healthtech startup in Europe, eight will say Berlin, one will say London, and one will whisper Lisbon for “quality of life reasons”. They’re all partially right and all are missing the bigger picture.

Europe isn’t one market. It’s 27 regulatory fiefdoms, three reimbursement philosophies, and a few hundred interpretations of GDPR. Your success depends less on your pitch deck and more on which country actually wants what you’ve built.

Below is your 2025 market map, written for people who need real answers: founders choosing their first market, investors analysing expansion, and operator-types who enjoy pain.

1. France

The most healthtech-friendly major market in Europe

Why France works

Strong government buy-in for digital health.

Funding muscle: Bpifrance, EU4Health, France 2030.

Single-payer structure = easier national rollout.

PECAN (the DiGA-like pathway) actually works.

Best for

Digital care delivery, AI diagnostics, practice management, DTx reimbursement plays.

If your solution is… Data heavy → Nordics / Baltics Reimbursement heavy → France / Germany Consumer-forward → UK Hardware + software → Switzerland / Ireland Cost-sensitive early-stage → Poland / Romania / Spain / Portugal

Europe rewards founders who pick the right first country — not the closest or the coolest. Start where the system actually wants what you’re building.

Europe HealthTech Market Selection Table (2025)

Region

Best For

Strengths

Risks / Caveats

France

DTx, diagnostics, digital care

Strong reimbursement, centralised system, public funding

Bureaucracy and long cycles

Nordics

Remote monitoring, preventive care, data platforms

Oncology operating systems, perioperative risk AI and pre-CT stroke triage all raised fresh capital this week, while Brussels and Munich quietly tightened the screws on AI compliance and imaging vendors celebrated a shiny new CE mark.

People on the move

Ergea Group (Luxembourg) New CEO for pan-European imaging & cancer care

Ergéa, a Luxembourg-based pan-European provider of diagnostic imaging and cancer care services, has promoted David Rolfe from UK CEO to Group CEO and appointed Mark Graves as the new CEO of Ergéa UK, signalling a more integrated European growth push in imaging and radiotherapy infrastructure.

Restore Medical (Israel): ex-Medtronic dealmaker takes the chair

Heart-failure device company Restore Medical (Israel, backed in part by the European Innovation Council Fund) has appointed Chris Cleary, former SVP Corporate Development at Medtronic and architect of the Covidien mega-deal, as chairman of the board to guide its transcatheter heart-failure therapy through advanced US and global clinical development.

Money flows

Gosta Labs (Finland) €7.5M seed, oncology AI operating system Helsinki-based Gosta Labs raised a €7.5 million seed round, led by Voima Ventures with COR Group, the Aho family, Reaktor and other angels, to scale its oncology-focused AI operating system that turns each patient encounter into structured data, slashes documentation time and links care decisions to international treatment guidelines. The company plans to deepen medical-device-grade development and expand deployments across Europe, the Baltics and Australia.

Noteless (Norway) €3.5M to fight doctor burnout Oslo-based Noteless, a Norwegian HealthTech startup automating clinical documentation and task management, closed a €3.5 million round to tackle physician burnout by cutting admin time in hospitals and clinics; the investor syndicate includes People Ventures and Alliance Venture, with the company targeting broader Nordic and European rollout.

Healthplus.ai (NL) €2.3M late-seed for perioperative risk prediction AI Amsterdam-based Healthplus.ai raised €2.3 million in a late-seed round led by Elevating Capital and co-led by LUMO Labs, with ROM InWest and Pathena among the participants, to expand PERISCOPE®, its ISO- and CE-certified AI system that predicts post-surgical infection risk and suggests mitigation strategies for surgical teams. The funding will support deeper EHR integrations (Epic, Cerner, ChipSoft), further model development across perioperative pathways and broader roll-out in Europe plus FDA clearance work for the US.

AI-Stroke (France) $4.6M seed for pre-CT stroke triage Paris-area medtech AI-Stroke secured a US$4.6 million seed round led by Heka (Newfund VC) with Bpifrance and angels, to advance an “AI neurologist” that runs on smartphones or tablets for pre-hospital stroke triage, analysing 30-second video of facial symmetry, arm movement and speech. The capital will fund FDA regulatory work and multisite clinical studies in leading US stroke centres, with the company also adding a heavyweight international stroke advisory board.

On the press

TÜV SÜD launches voluntary EU AI Act conformity certificates

TÜV SÜD announced new services for early, voluntary conformity certificates under the EU AI Act (Regulation (EU) 2024/1689), offering manufacturers of AI systems including high-risk use cases in medicine and medical devices an independent review of technical documentation and partial compliance ahead of mandatory assessments. The program covers gap assessments, training and an “Attestation of Conformity,” aimed at helping companies get AI products AI-Act-ready before notified bodies are fully designated.

GE HealthCare wins CE mark for Omni 128 cm total-body PET/CT

GE HealthCare received CE mark for its Omni 128 cm total-body PET/CT system, enabling commercialisation in the EU of an ultra-long axial field-of-view scanner intended to improve sensitivity, enable low-dose protocols and support advanced oncology and theranostics workflows. The platform is pitched at high-throughput cancer centres and research hubs across Europe.

MHRA outlines “innovative approaches” to medtech regulatory reform

The UK MHRA’s MedRegs blog set out its latest thinking on medtech regulatory reform, highlighting more agile statutory instruments, innovation-friendly approval routes, and closer alignment with international partners for medical devices and IVDs. For EU-facing companies selling into the UK, the piece is a useful signal on future reliance routes and how sandbox-style approaches may coexist with post-market vigilance expectations.

One thing to remember

AI-heavy clinical tools are still getting funded from oncology operating systems to perioperative risk prediction and pre-CT stroke triage. This week’s TÜV SÜD and MHRA moves are a clear reminder that in Europe, “AI-first” now has to mean “AI-and-compliance-first.”

For founders, the competitive edge is shifting toward teams that can show device-grade evidence and be visibly AI-Act-ready long before their product hits a hospital PACS or EHR.

If you work in HealthTech in Europe, you’ve probably noticed something strange. 2024 felt like the world was ending, yet the actual numbers say something very different. Capital didn’t disappear — it simply stopped tolerating nonsense.

Now, in 2025, the money is flowing again, and aggressively so. But it’s flowing selectively.

2024: The Great Reality Filter

Forget the headlines about a funding collapse. What actually happened in 2024 was a reset of expectations. Investors didn’t stop writing cheques, they just stopped writing them for half-baked pitch-deck poetry.

A study analysing ~1,300 funding rounds across European biotech, medtech and digital health showed fewer deals, but bigger ones. Median pre-seed funding actually rose ~15.7% YoY to around €870K, which doesn’t sound like panic to me.

And Q3 2024 alone brought nearly US$2B in HealthTech investment.. The hubs were the usual suspects: UK, Germany, France, with Spain, Portugal and the Netherlands quietly moving up the table.

The hottest segments? Oncology, biotech and AI-powered diagnostics: areas where outcomes are measurable and regulatory paths exist.

Karista summed up the year perfectly: a “reality filter”.

It was not a crash, but a sorting mechanism. The pretenders left the room, the contenders stayed.

2025: Capital Is Back, Smarter

Then 2025 arrived and the mood changed fast.

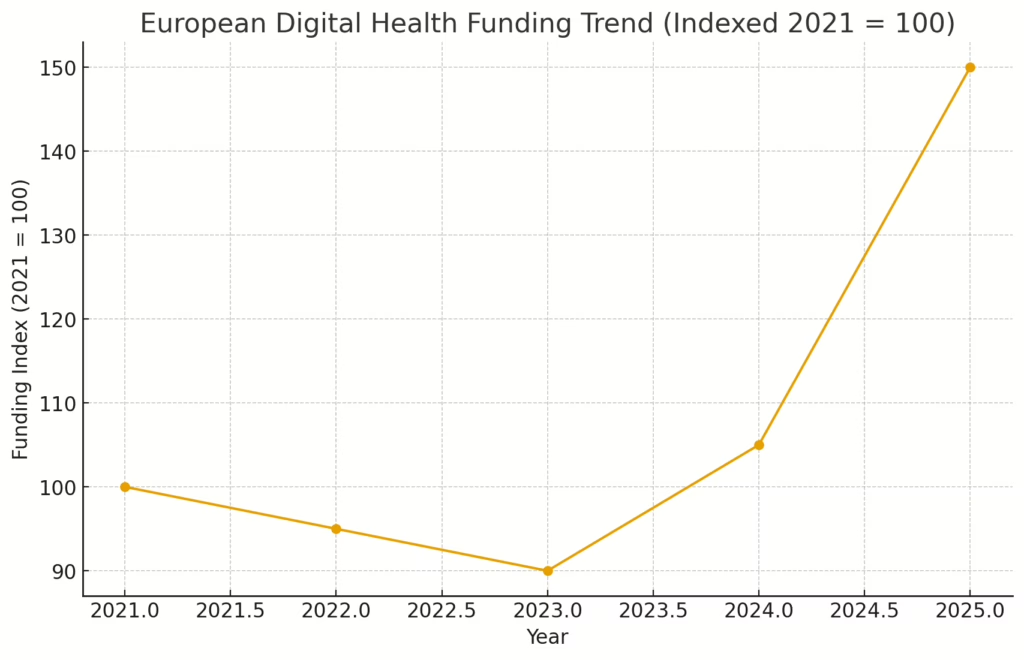

According to Galen Growth, European digital health funding grew 52% YoY in H1 2025, totalling around US$3.4B across 182 deals. Europe is representing 26% of global funding

Figure 1. European Digital Health Funding Trend 2021–2025 (Indexed) Indexed view using 2021 baseline of 100. 2025 funding growth (52% YoY, US$3.4B H1) based on Galen Growth. 2021–2024 values illustrative, derived from partial public snapshots. Source: disrupting.healthcare

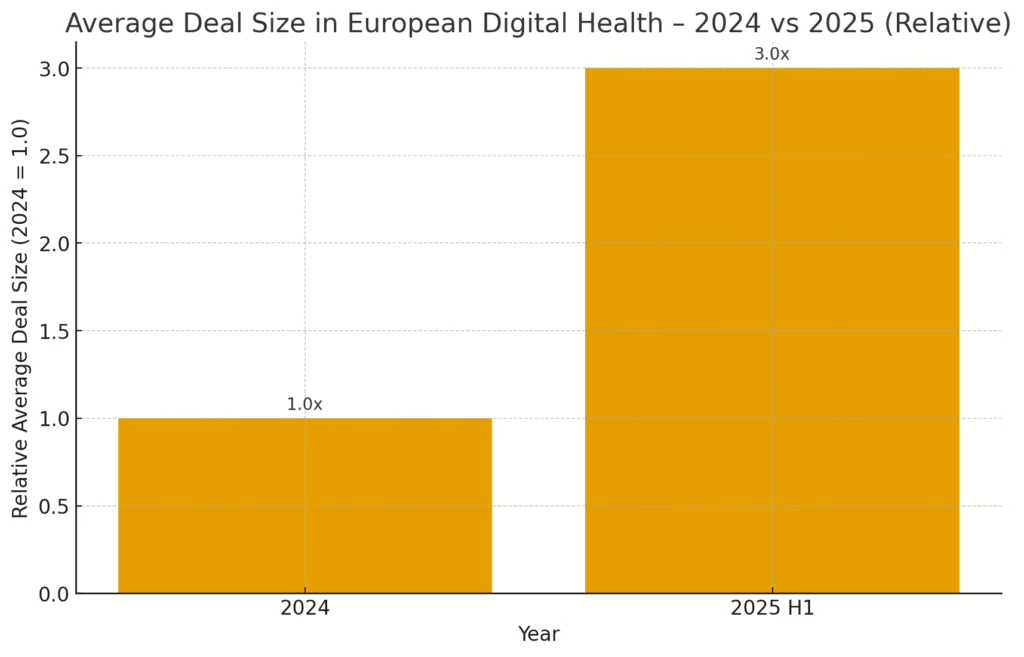

Figure 2. Average Deal Size — 2024 vs 2025 (Relative) Based on publicly reported 3× YoY increase in average deal size (Galen Growth, Healthcare.Digital). Source: disrupting.healthcare

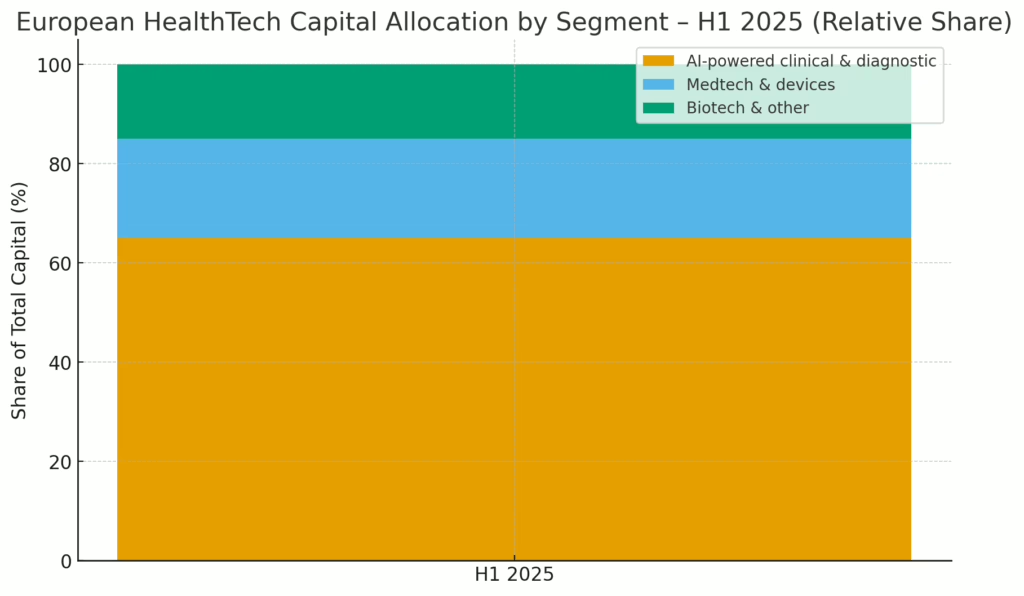

Even more striking: ~65% of all capital went to AI-powered clinical and diagnostic platforms.

Figure 3. Capital Allocation by Segment — H1 2025 ~65% of capital allocated to AI-driven clinical & diagnostic platforms (Galen Growth, H1 2025). Source: disrupting.healthcare

This isn’t a hype revival, but it’s conviction capital. Investors aren’t betting on stories. They’re betting on proof.

The Difference in One Sentence

2024 sorted the real players from the noise. 2025 is paying the real players.

Metric

2024

2025

Deal flow

Reduced volume

Clear acceleration

Average deal size

Reduced volume

€16M

Funding Focus

Biotech, oncology, med-device

AI-clinical & diagnostic

Investor tolerance

Traction required

Validation required

Entry barrier

Brutal

Still high, but capital available

Capital geography

UK, DE, FR

Broader pan-EU activity

What to Do With This Information

If you’re a founder:

If you have validation: raise now.

If you only have a concept deck: don’t waste everyone’s time.

Mix non-dilutive + VC — it’s no longer optional.

If you’re an investor:

Europe is still undervalued vs the US — genuine upside exists.

Secondary acquisitions are coming.

AI is not a theme — it’s now an allocation mechanism.

It’s not 2021 again. 2025 is healthier, clearer, and honestly, more exciting.

Data Methodology & Transparency

The charts included in this article illustrate directional trends in European HealthTech funding rather than precise historical totals. Publicly available data does not provide continuous, fully aggregated funding records across all HealthTech sub-segments (digital health, medtech, diagnostics, biotech) from 2021 through 2024.

The indexed 2021–2025 funding trend chart is a normalized illustrative representation designed to highlight directional recovery and acceleration rather than exact historical volumes. Earlier periods (2021–2024) are estimated using partial public snapshots and normalized to a 2021 baseline of 100 to enable comparison.

The chart communicates trajectory, not absolute values. Where precise historical figures are required (e.g. investor deck, financial report), a consolidated dataset should be constructed from Dealroom / PitchBook / CB Insights / Crunchbase Pro and national grant databases.

Robotics bags big money, IVF gets an automation CE mark, and UK regulators sketch next steps for AI in care.

People on the move

Distalmotion (Switzerland) Chas McKhann becomes Executive Chairman alongside a $150M raise; focus is US growth while keeping EU base in Lausanne.

Money flows

Distalmotion (Switzerland) $150M, Series G / growth; scaling DEXTER® surgical robotics with ASC push and US commercial build-out.

Sofinnova Partners (France) — €650M, flagship Capital XI; early-stage focus in medtech/biopharma, active deployment underway.

On the press

• Overture Life (Spain) CE markfor DaVitri™, billed as the first automated device cleared in the EU or US for vitrifying unfertilised eggs; EU commercial rollout begins.

• Cardiovalve (Israel) CE file submitted for transcatheter tricuspid valve after positive TARGET study interim; EU approval process initiated.

• JenaValve (Germany) 1,000th case with CE-marked Trilogy™ TAVR for aortic regurgitation/stenosis, signalling steady EU adoption.

Capital and credibility still move together: big-ticket robotics funding and a heavyweight €650M early-stage fund arrived the same week that EU-relevant CE activity and the UK’s AI-in-health policy guardrails advanced. It is an evidence that clear regulatory paths plus deployment stories are what unlock cheques right now.

A compact week: small but pointed rounds in diagnostics and patient safety, a urology partnership scaling across EMEA, radiosurgery planning cleared on both sides of the Atlantic, and a headline corporate restructure.

People on the move

Exstent (UK) – Vascular surgeon Matt Thompson becomes CEO to drive commercialization of patient-specific aortic support.

Money flows

Self.co, formerly known as Allergomedica, (Lithuania) a €2.56M mixed grant + venture to scale molecular allergy testing and expand into the UK, Ireland, Austria and Germany; grant component from Innovation Agency Lithuania.

Enteral Access Technologies (UK) a £500K bridging round to scale DoubleCHEK, its CO₂+pH nasogastric tube placement safety device; building UK adoption and early EU rollout.

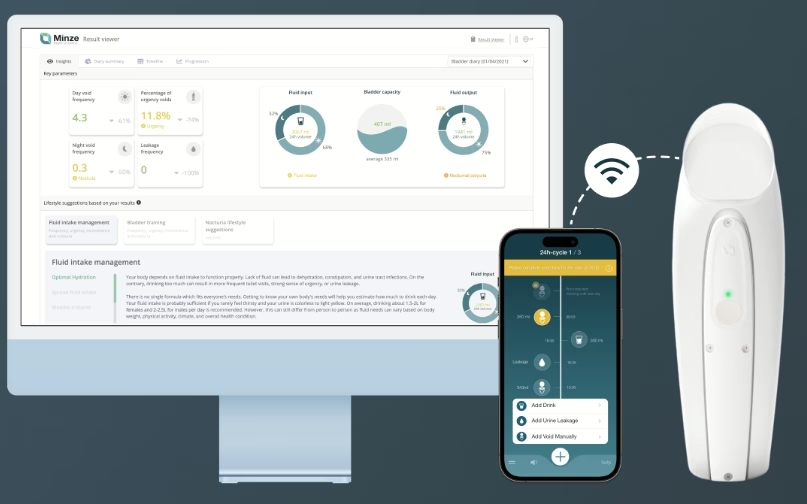

Minze Health (Belgium) × Medtronic: a three-year EMEA partnership to offer Minze’s automated bladder diary (Diary Pod) to patients receiving Medtronic sacral neuromodulation therapy; strengthens digital urology care pathways.

On the press

• ZAP Surgical: ZAP-Axon radiosurgery planning system receives both EU CE certification and US FDA 510(k); enables clinical use across the EU and US.

• Siemens to deconsolidate Healthineers: Siemens plans a direct spin-off of 30% of its ~67% stake to shareholders, cutting to ~37% and targeting <20% medium-term; expect governance/strategic autonomy effects for a core European medtech anchor.

Seed-stage cash is trickling into practical, reimbursable workflows (diagnostics, patient safety) while scale comes from channel partnerships and regulatory wins; design for distribution and evidence now so you’re ready when the capital tides turn.

The VCs, public funds, and CVCs writing cheques in European healthtech (2025 edition)

Healthtech funding in Europe is accelerating again. After a cautious 2023, investment rebounded to $4.8 billion in 2024, and Q1 2025 alone brought in $4.3 billion. Healthtech now captures 30 to 35% of all venture activity across the continent. But who’s actually writing those cheques?

This post breaks down the capital stack behind Europe’s digital health growth: venture capital, public funds, and corporate/strategic investors. Whether you’re raising or deploying capital, here’s who you need to know in 2025.

1. Venture Capital: Still the Primary Engine

Venture capital is behind most of the major healthtech rounds in Europe. From seed to Series C, VCs provide the scaling fuel, validation, and network access.

Top 5 VCs Investing in European HealthTech:

Sofinnova Partners: Paris-based life sciences fund active in healthtech, diagnostics, and therapeutics.

Octopus Ventures: UK fund with a strong healthtech thesis, including femtech and digital care.

Speedinvest: Vienna-based early-stage investor with a focus on digital health and care platforms.

EQT Life Sciences: Nordic growth-stage investor in diagnostics, medtech, and health platforms.

Calm/Storm Ventures: Focused on pre-seed and seed-stage digital health across underserved areas like paediatrics and mental health.

Who are the best VCs for digital health in Europe?

Those five are consistently active in 2024-25, spanning early to growth-stage capital.

2. Public & EU Funding: De-risking and Catalysing Growth

Public funding rarely leads rounds, but often enables them. Grants, co-investments, and match funding are key to bridging early clinical stages and reimbursement pilots.

Key Public Funding Sources for HealthTech in Europe:

Horizon Europe: EU R&D programme with dedicated tracks for health and medtech.

EU4Health: €5.3 billion programme for health system resilience and digitalisation.

Bpifrance: France’s national investment bank, active in medtech, digital health, and AI.

Innovate UK: Grant and co-investment body supporting UK healthtech pilots and R&D.

Can you get EU grants for a healthtech startup?

Yes. Programmes like Horizon Europe, EIC Accelerator, and EU4Health fund clinical validation, digital health infrastructure, and medtech scale-up.

3. Corporate Venture & Strategic Investors: Validation with Capital

CVCs and strategic investors are increasingly active in Series B+ deals. They offer more than capital, including access to clinical settings, distribution, and potential M&A.

Key Corporate Venture Funds:

Philips Ventures: Investing in digital diagnostics, patient monitoring, and chronic care.

Do corporates invest in digital health startups in Europe?

Yes. In 2025, CVCs from pharma, medtech, and insurance are increasingly co-investing in digital health.

Estimated Funding Breakdown (2025):

Source

Share Estimate

Role

Venture Capital / PE

65–75%

Lead rounds, scale capital

Public Funds / Grants (EU + National)

10–20%

Early-stage, pilots, non-dilutive

Corporate / Strategic / CVC

10–15%

Strategic fit, late-stage, distribution

Insight: Most healthtech rounds in 2025 involve blended capital: a VC lead, public match-funding, and a strategic partner.

Strategic Takeaways

Founders: Match your capital to your stage. Grants and public co-investments work best pre-revenue or pre-regulatory. Investors: Watch for startups with public funding traction—often a good de-risking signal. Operators: CVCs are gatekeepers to reimbursement and go-to-market. Engage early, but be realistic on timing.

Next up: How the funding mix changed between 2024 and 2025, and what it signals about the future of EU healthtech capital.

Cardio-adjacent robots, workflow expansions, and device commercialization: this week mixes a new fund backing medtech, a fresh CE mark, and EU market-surveillance tidings.

United Founders (Luxembourg) €80M early-stage fund, cheques up to €1M, targeting AI, hardware, dual-use and medtech; early health bet includes Germany’s Every Health. Expect more operator-led tickets into clinical workflows.

Holi (Poland) €3M Seed; digital obesity clinic. New markets in EU on deck; product build around data-driven care pathway.

Nanox (Israel) ↔ EXRAY (Czech Republic) Distribution partnership for Nanox.ARC 3D imaging across Czech Republic; leverages recent EU CE mark to widen footprint. Useful read-through for cost-sensitive imaging buyers in CEE.

On the press

• Nitinotes (Israel) – CE mark for EndoZip, an automated suturing system for endoscopic sleeve gastroplasty; sets up EU commercialization of obesity intervention between drugs and surgery.

• EU #MedSafetyWeek Commission’s health agency Hadea spotlights JAMS 2.0, the joint action strengthening medical device/IVD market surveillance, inspections and data exchange across Member States. Signal: more coordinated enforcement under MDR/IVDR.

• Urteste (Poland) launches European multicenter clinical study of Panuri, an oncology test; another CEE diagnostic attempting EU-wide validation.

One thing to remember

Obesity and imaging drove the week: fresh capital for a Polish digital clinic, a CE-marked automated ESG platform, and a Czech distribution deal show Europe’s buyers want scalable, cost-sensitive interventions. Pair commercialization sprints with the EU’s tighter market-surveillance push to avoid regulatory surprises later.

AI pathology and precision health get fresh fuel; MDR CE marks stack up; MHRA drops safety signals and an IDAP tweak—another week of pilot-to-product momentum.

People on the move

ViCentra (the Netherlands) Ex-Dexcom and Medtronic leaders join to scale Kaleido across Europe; Karen Baxter becomes SVP Sales, Europe; Jay Little becomes VP Strategy & Business Development.

• Lumendi EU MDR CE mark for DiLumen™ EZ¹ and DiLumen™ C¹ endotherapy devices; enables EU commercial distribution.

• Bot Image MDR CE mark for ProstatID® AI prostate MRI software, opening European market access; product is FDA-cleared in the U.S.

• MHRA — October Safety Roundup and Field Safety Notices published; useful for vigilance teams.

• MHRA — IDAP update: UCNA extension for HistoSonics’ EDISON™ ultrasound ablation system; worth tracking alongside EU MDR routes.

One thing to remember

Regulatory momentum matters: CE marks keep landing while the UK fine-tunes access pathways, and capital is returning tohiow focused clinical AI and women’s health sensors. Founders who tie clinical utility to crisp EU/UK access narratives will convert faster to distribution.

Valuation isn’t everything but in healthtech, it tells you who’s still scaling

Let’s not pretend valuation is the ultimate success metric. But it is a decent proxy for where capital, confidence and commercial traction are flowing. Especially in a market as fragmented and overregulated as European healthcare.

The 2025 leaderboard of Europe’s top 10 most valuable healthtech companies.

Not biotech. Not pharma. Just tech-enabled health. Companies at the intersection of software, care and medical delivery models. Most are private. A few are flying under the radar. And yes, Finland opens the list.

Valuation: US$11 billion (Sep 2025) What it does: Smart wearable ring + health analytics Why it matters: Europe’s wearables play moving into serious health data.

Valuation:US$6.4 billion (2025 ranking) What it does: Appointment booking and telehealth platform for European health systems. Why it matters: A dominant platform reaching scale across French & German markets, signalling what digital health infrastructure looks like in the EU.

Valuation: US$4 billion (June 2025 funding round) What it does: AI-enabled digital therapy / musculoskeletal care Why it matters: Bridges digital therapeutics and service delivery with high value healthcare cost savings.

Valuation: Reported ~US$2 billion What it does: Telemedicine/virtual primary care (marketed as “Livi” in UK/France) Why it matters: One of the larger pan-European virtual care plays.

Valuation: Reported >US$1 billion (source) What it does: Tech enabled home care & community services Why it matters: A service delivery business scaling across UK homecare, a difficult but high impact node of the health system.

Valuation: ~US$1 billion What it does: Women’s health (cycle tracking, fertility, health analytics) Why it matters: Rare consumer digital health “scale” platform in Europe with global ambitions.

Valuation: ~US$1.8 billion What it does: Full body scanning diagnostics with AI Why it matters: Diagnostics and proactive screening is one of the less hyped but high upside segments in EU healthtech.

Valuation: ~US$600 million (estimate) What it does: Wearable insulin delivery device + patient engagement Why it matters: Device + digital combo in chronic disease management

Valuation: ~US$300 million (estimate) What it does: Continuous blood pressure monitoring without cuffs Why it matters: Remote monitoring is crowded, but clinically meaningful, reimbursable models still rare.

Valuation: ~US$150 million (estimate) What it does: Smart ambient care sensors for elderly living at home Why it matters: A realworld aging play; modest valuation, but high relevance for Europe’s demographic shift.

What this list tells us?

Valuation follows integration. The highest valued companies are those who figured out how to embed into care delivery systems, not just launch a product or service. It’s not just software. Many of the names here incorporate hardware or device components, but the business model leads with experience, outcomes, and scale. Europe has range. From Portugal to Sweden to France, the value creation is not limited to London/Berlin (though they still matter). But caution remains. Private valuations are fluid. Some said “decacorn” for Oura a year ago; latest official validated valuation is half of it at around ~$5.2bn the jump to ~$11bn comes from news speculation.

One Last Note

This list isn’t final, and it will change, maybe an hour after the publication. Private valuations shift. Some firms may consolidate or pivot. But if you’re looking to invest, compete or expand — these are the healthtech companies dominating European healthtech headlines for now.

Next up: where the money’s coming from — and who’s still writing the big cheques.